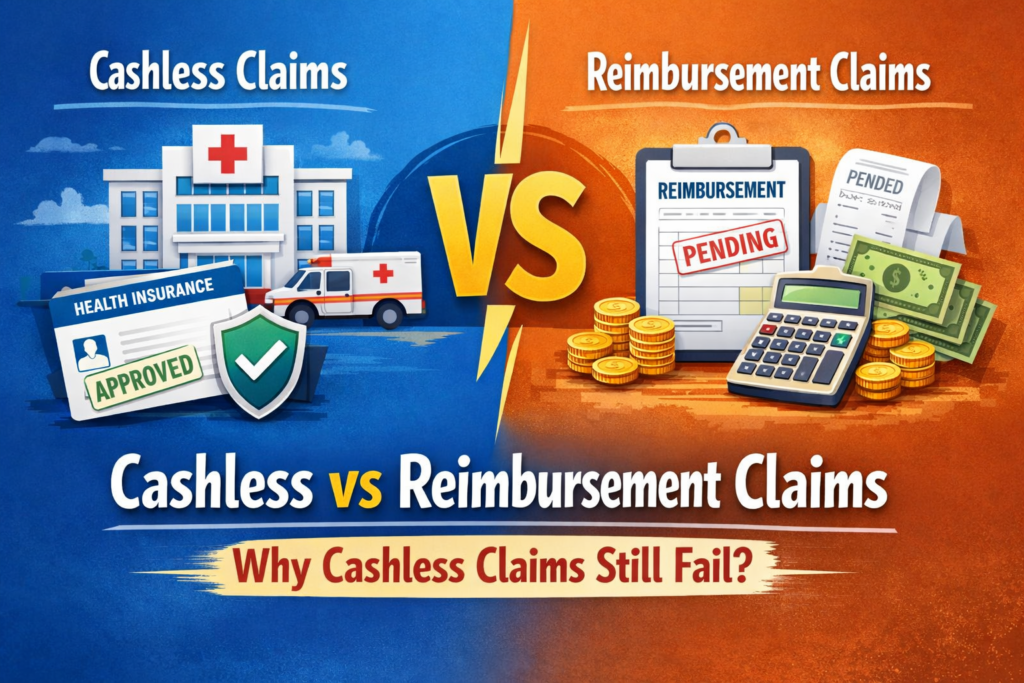

Cashless vs reimbursement claims are two common ways policyholders use health insurance during medical emergencies. Health insurance helps people handle medical costs during emergencies, and one useful feature provided by many insurers is the cashless claim option. This system allows insured individuals to receive treatment without paying the full hospital bill upfront.

Also read: Why Health Insurance Claims Get Rejected in India

Health insurance helps people handle medical costs during emergencies. A useful feature provided by many health insurance companies is the cashless claim option. This system lets insured individuals get medical treatment without paying the full bill at the hospital in advance.

Yet, some policyholders feel confused or frustrated when their cashless claim gets delayed or denied even when their health insurance policy is valid. Knowing how cashless claims differ from reimbursement claims can help people prepare to tackle these challenges better.

A cashless claim lets policyholders get treated in a hospital from the insurer’s network without needing to pay the total bill upfront when they are discharged.

Here’s how it works:

The policyholder covers non-covered costs, deductions, or any charges over the policy’s limit.

A reimbursement claim works in a different way. Here, the policyholder pays the hospital expenses first and then files a claim with the insurance company to get the money back.

The usual steps in the reimbursement process are:

People use reimbursement claims often when they get treated at a non-network hospital or if the cashless option doesn’t get approved.

Cashless claims are made to simplify things, but they can still fail sometimes because of a variety of reasons.

Insurers offer cashless claims at their listed network hospitals. If someone gets treated at a facility outside this list, they need to file a reimbursement claim instead.

Health insurance policies often enforce waiting times for some conditions. These may cover:

If you get hospitalized during this waiting time, the insurer might refuse your cashless claim.

Hospitals must share a pre-authorization form with the insurer in advance for planned medical treatments or procedures. Missing or incorrect paperwork can lead to problems.

If the request lacks necessary details or skips key medical information, the insurer might hold off or turn down the cashless approval.

Insurance policies have specific exclusions and restrictions. When a treatment includes:

the insurer could refuse the cashless claim.

When there is a mismatch in:

the insurer might ask questions or deny approval until things are cleared up.

Cashless approvals can also fail if:

Having your cashless claim denied doesn’t always mean you lose the chance to get your claim approved .

Often, you can still make a reimbursement claim after getting discharged. You just need to send all the required paperwork to the insurance company. They will check the claim by comparing it with the rules of the policy and the details you submitted.

Taking some simple steps can help you avoid cashless claim-related issues.

Knowing these steps can reduce unnecessary stress when facing medical emergencies.

Insurance claims during medical emergencies can create a tough time for families and policyholders.

At Eternity Claim Solutions, we help you understand your insurance plan and solve issues with claims. We go over your policy, figure out why claims might get delayed or rejected, and walk you through the steps to fix the problem.

We aim to give clear guidance that helps policyholders understand their rights and options better.

Both cashless and reimbursement claims exist to help policyholders handle healthcare costs. But a claim’s outcome relies on different things like the policy terms, network hospitals proper paperwork, and medical information shared.

Knowing how these claim methods function allows policyholders to sidestep surprises and make smarter choices when using their health insurance.